Warren Buffett never fails to recommend it and 90% of US fund managers struggle to beat it. If you’re wondering what this miracle investment is, it’s the US S&P 500 index. Indian investors will soon have the opportunity to buy this US benchmark locally with Motilal Oswal AMC launching an open-end index fund replicating it – The Motilal Oswal S&P 500. The fund will carry a total expense ratio of 1% under the regular plan and 0.5% under the direct plan, with minimum investments of Rs 500.

Warren Buffett never fails to recommend it and 90% of US fund managers struggle to beat it. If you’re wondering what this miracle investment is, it’s the US S&P 500 index. Indian investors will soon have the opportunity to buy this US benchmark locally with Motilal Oswal AMC launching an open-end index fund replicating it – The Motilal Oswal S&P 500. The fund will carry a total expense ratio of 1% under the regular plan and 0.5% under the direct plan, with minimum investments of Rs 500.

The NFO opens on April 15, 2020. Should you bite?

What’s in it?

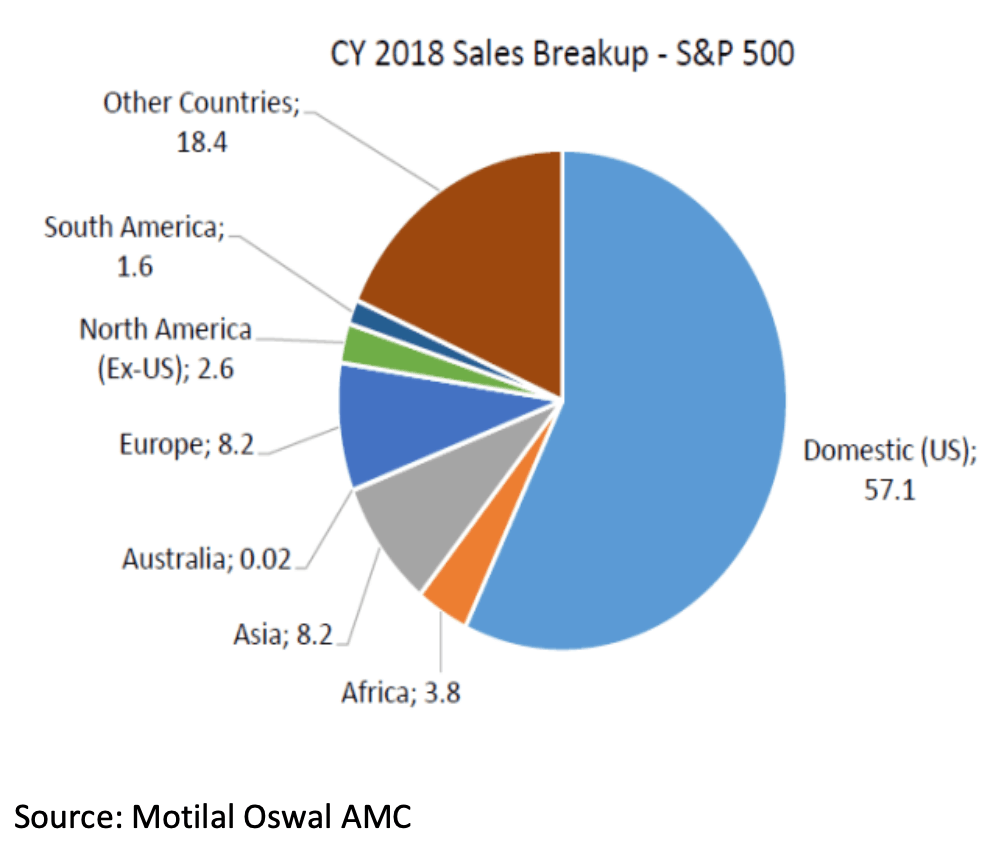

The S&P 500 index is a free-float market cap-weighted index made up of the 500 most liquid large-cap names in the US market. The index covers 82% of US market capitalisation. Nearly $10 trillion of assets globally are benchmarked to it, with index funds valued at $3.4 trillion tracking it. Compared to the Nasdaq 100 or Dow Jones Industrial Average, the S&P 500 offers a much wider coverage of the US market, representing both industrial and technology names across eleven sectors. The index currently features 505 stocks with a total market cap of $22,569 billion.

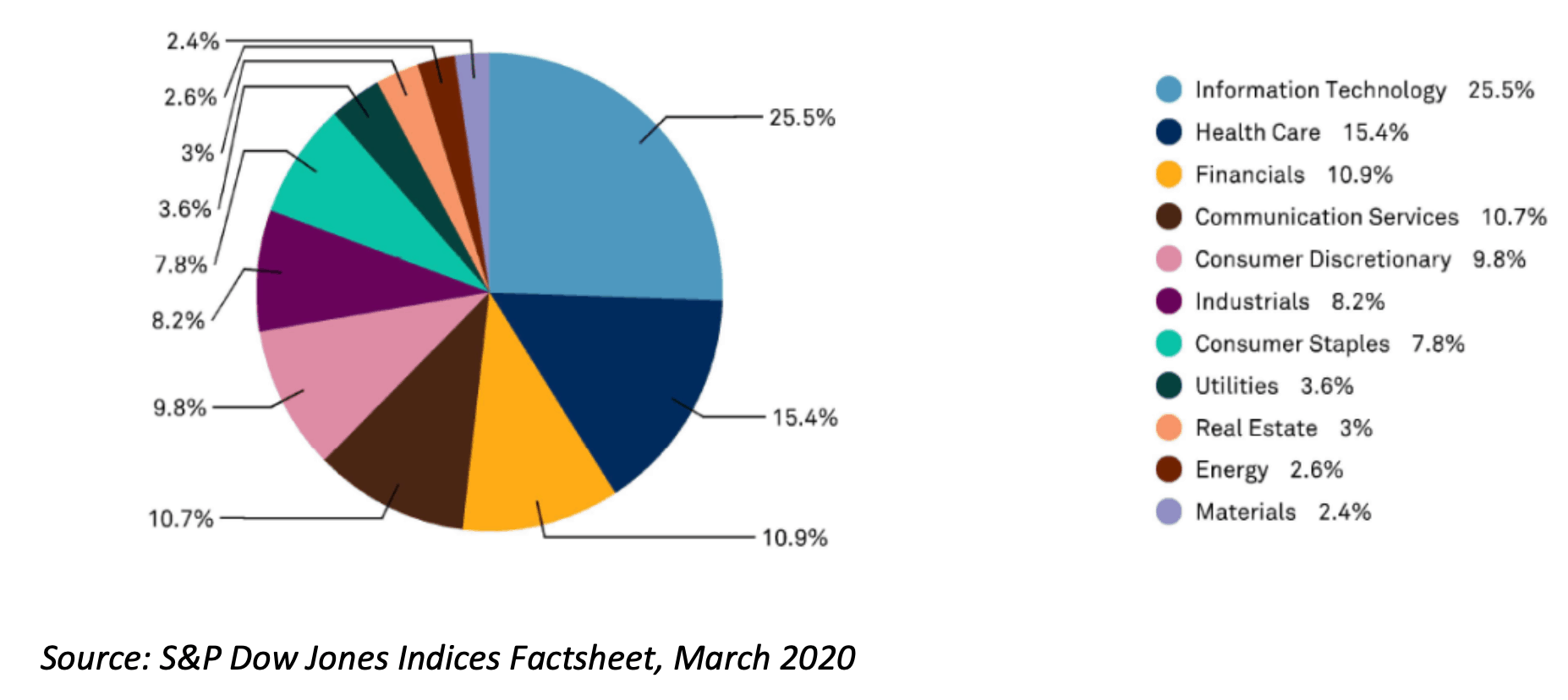

Compared to Indian indices such as the Nifty50 or even the Nifty500, the US S&P 500 is a more diversified index. Its top sector – Information Technology – is at 25.5%, followed by healthcare (15.4%), financials (11%), communication services (10.7%) and consumer discretionary (9.8%). Its top ten holdings making up a 25.4% weight. India’s Nifty500 features a bigger weight of 32% weight to its top sector financial services and top ten stocks take up a 44% weight.