Last week we wrote about the performance of equity funds in 2019. This week we’ll discuss about the fund category that made the most number of headlines in pink papers – debt funds. The 2018 fallout of the IL&FS debacle carried itself into 2019, causing downgrades and defaults in several NBFCs, notably DHFL.

Last week we wrote about the performance of equity funds in 2019. This week we’ll discuss about the fund category that made the most number of headlines in pink papers – debt funds. The 2018 fallout of the IL&FS debacle carried itself into 2019, causing downgrades and defaults in several NBFCs, notably DHFL.

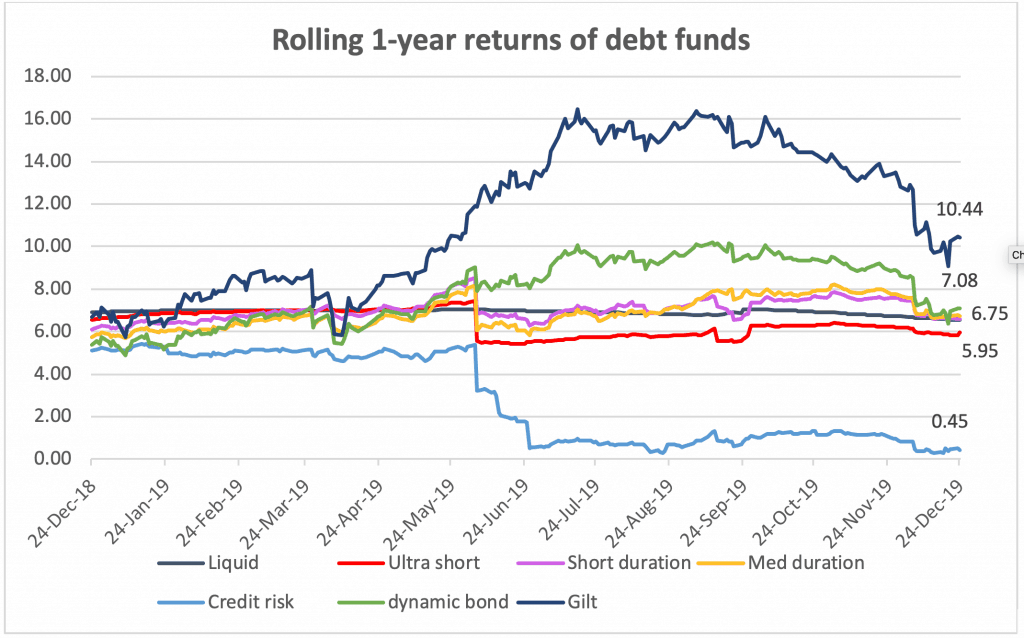

Complex webs, woven by corporate group holdings, also broke, with the Essel group (Zee group) entering into informal agreements with AMCs, requesting for their patience with the amount lent. That debt funds held instruments in telecom companies, which are in dire state for a different reason, further caused panic. Amidst all this turmoil, how did debt funds fare in 2019?

Here’s a summary of the year’s performance

- On a point to point basis, funds that follow a duration strategy (take interest rate calls) did well, as the series of rate cuts eased yields (causing bond prices to rise) providing gains to fund NAVs. Categories such as gilt and dynamic bond benefitted the most from this rally. Others such as corporate bond and short duration that held short to medium term bonds also marginally benefitted from the price rally in debt. You can see in the table below that these categories returned higher than the previous year.