Thanks for visiting PrimeInvestor!

Hi, My name is Srikanth Meenakshi - I am a co-founder at PrimeInvestor. Thanks for visiting. After reading this article, I welcome you to check out our offerings here. You can also learn more about our team . And, you can start using our services by signing up for a trial.

We help you be careful with your money. Stay informed. Sign up today!

(With inputs from Aarati Krishnan)

Do you remember the last time that the Nifty fell over 500 points on a single day? Wondering if it was in 2008? No, because it never did in absolute value terms. That’s what makes March 9, 2020’s Nifty fall so scary. And because it is scary, many investors are taking the flight to safety route, looking for safe debt options or piling on to gold instead of volatile equities.

But at Primeinvestor, we think this is the time to raise allocations to equities and not to take refuge in debt or gold. Here’s why and where to invest.

Not the time to chase gold

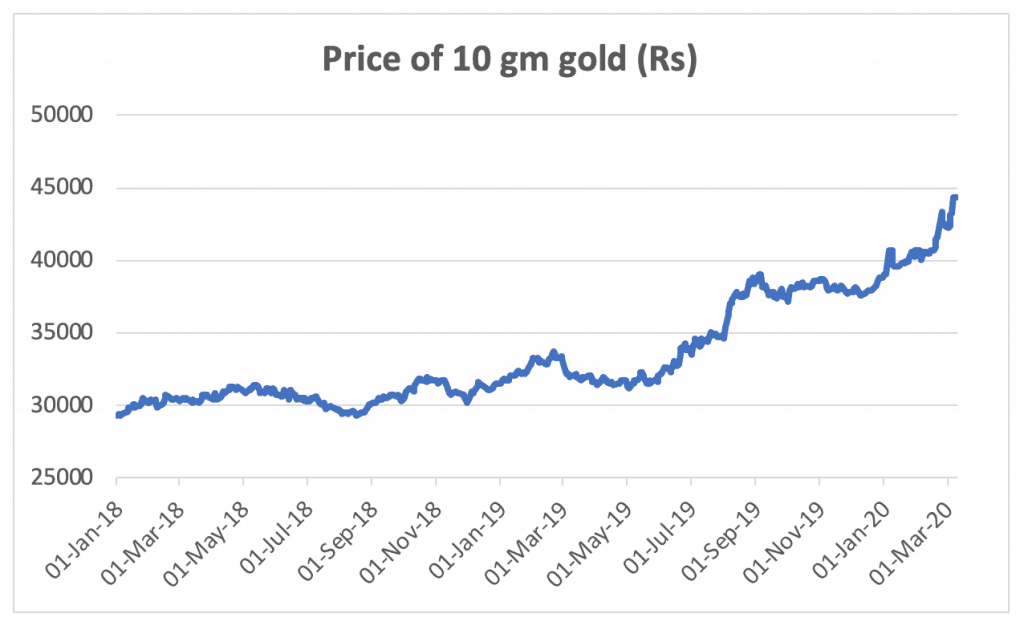

With the deadly cocktail of coronavirus and recession fears hitting global markets, gold has been the recent hero. Globally gold prices have now gone back to highs of 7 years ago (2013) but in India, thanks to Rupee depreciation, gold is at a life high. From the last low of August 2018, gold has risen an absolute 51% or 25% annualized till March 9, 2020. About 11% of those gains have come after the news of coronavirus gripped the market in the latter part of January 2020.

But gold’s recent performance is in itself a good reason to stay away from raising allocations to it, in your portfolio. Chasing assets that have performed well in the recent past always leads to sub-par returns in the long run. What’s more, the key role of gold in any portfolio is that of a hedge, an insurance. You don’t take an insurance after the event has transpired because that’s when premiums are sky-high. The purpose of insurance is to take cover before risks crop up. Yes, gold will likely rally for a while until the uncertainty of coronavirus or recession fears linger. But as an entry point, this is the wrong time to raise allocations to gold.